Most published research about warehouse and inventory software is written by the companies that sell it, and it usually says the same thing: buyers want efficiency, visibility, and scale. That is true and useless.

We had access to something more specific. Between February 2025 and May 2026 we recorded 76 sales conversations with mid-market eCommerce merchants who were actively evaluating new inventory, order, and warehouse management software. These were not surveys. They were the unscripted, hour-long conversations where a business owner or operations lead explains, in their own words, what is broken, what they run today, and what they can afford. Together the transcripts run to 460,694 words, an average of 6,062 words per conversation.

This is what those conversations show when you count them instead of quoting the most dramatic one. Where a finding could be measured two different ways, both numbers are reported and labeled, because the honest version is more useful than the impressive one.

Methodology, up front

The sample. 76 recorded sales-demo conversations with prospective buyers of inventory, order, and warehouse management software. All 76 are non-empty and were analyzed. Conversations span 2025-02-17 to 2026-05-14.

The unit of measurement. Every percentage in this report is conversation-level: "X of 76 transcripts." A figure of 47 of 76 means the theme appeared in 47 distinct conversations, not that it was mentioned 47 times.

Two counting methods, always labeled. Some findings are counted by transcript text (the word or tool appears anywhere in the raw conversation, spoken by either party). Others are counted by structured extraction (a normalized read of what the prospect stated about their own situation: their pains, their current tools, their budget). The two methods disagree in predictable ways. Speech-to-text garbles brand names, so raw-text counts undercount tools like Cin7 (transcribed as "sin 7" or "sync 7") and Linnworks (which the transcript never captured cleanly at all). Extraction corrects those garbles but only captures what the prospect said about their own stack. We show both and tell you which is which.

What this sample is not. These are merchants who had already decided to evaluate new software, so they are self-selected toward dissatisfaction with their current setup. Each conversation was with a single vendor, so the buyer's framing of the market is partial. This is a benchmark of mid-market buyers in an active buying cycle. It is not a census of all merchants, and it is not a neutral product comparison. Read the numbers as "what buyers in motion look like," not "what the market believes."

Headline findings

Finding 1: Mid-market inventory still runs on spreadsheets

The single most common pain, by a wide margin, is manual and spreadsheet-based process. In 47 of 76 conversations (62%), the prospect described spreadsheets, Excel, Google Sheets, or manual workflows as a core problem in their own words. When counted more conservatively, by whether the word "spreadsheet," "Excel," or "Google Sheet" was spoken aloud at all, the figure is 26 of 76 (34%).

The gap between those two numbers is itself the finding. Many merchants do not say "spreadsheet." They say "we do everything by memory," or "none of the software communicates," and the manual reality sits underneath. The spreadsheet is not always named. It is almost always there.

"We're using Google Spreadsheet. So it's very cumbersome, it's very manual. Sometimes inventory goes missing, even though it's physically available... And sometimes inventory is gone and it's still represented on the sheet."

- perishable-meat food company

"Everything we're doing right now is by memory for the purchasing side. Everyone just calls somebody when they need something and orders it."

- steel-erection contractor

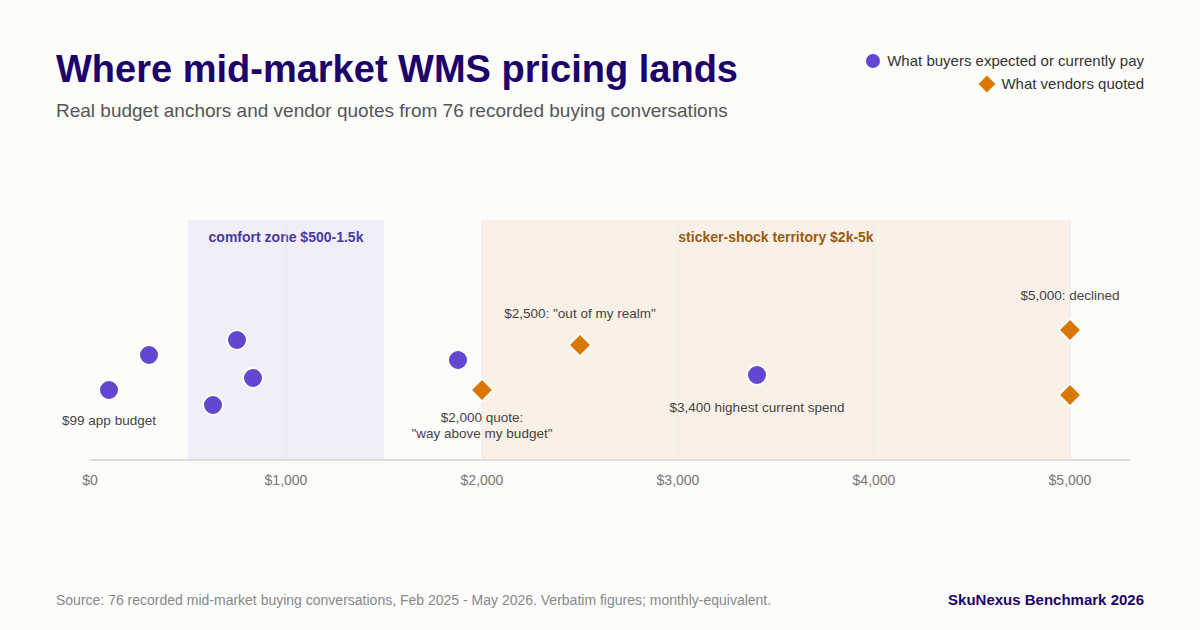

Finding 2: Buyers anchor low, and quotes above a clear threshold trigger sticker shock

Pricing is not a side conversation for this buyer. 66 of 76 conversations (87%) contained a substantive budget or pricing signal. 56 of 76 (74%) contained at least one dollar figure of $100 or more spoken in the raw conversation. And 49 of 76 (64%) contained an explicit price, cost, or budget objection.

The pattern in those signals is consistent enough to state plainly. Mid-market merchants repeatedly anchor their expectation between a few hundred dollars and roughly $1,000 to $1,500 per month. Quotes in the $2,000 to $5,000 per month range produced explicit sticker-shock reactions in at least 8 transcripts. Flat-rate, volume-independent pricing was repeatedly received as a strong positive; per-order fees were repeatedly received as a threat. The full verbatim anchors are in the pricing section below.

Finding 3: More than half name a specific tool they are trying to leave or integrate

41 of 76 conversations (54%) named at least one third-party warehouse, inventory, or shipping tool from a tracked list (counted by raw transcript text). Using the broader extraction method, which also captures incumbent ERPs and in-house builds, 71 of 76 (93%) have at least one existing or alternative solution on record. Almost nobody is starting from nothing. They are starting from something that no longer fits.

The most-referenced point solution is ShipStation, named in 15 conversations by transcript text and 14 by extraction. In several of those, it appears as an incumbent being pushed past its intended purpose, used as an order-management and shipping hub rather than a shipping tool. The full incumbent table is below.

Finding 4: This is a mid-market volume profile, with a seasonality tail

39 of 76 conversations (51%) stated a concrete order or shipment volume. Bucketed by typical daily volume:

| Daily order volume | Conversations | Share of the 39 who stated a figure |

|---|---|---|

| Under 100 orders/day | 16 | 41% |

| 100 to 999 orders/day | 21 | 54% |

| 1,000+ orders/day | 2 | 5% |

The median stated volume sits in the low hundreds of orders per day, roughly 3,000 to 9,000 orders per month. Stated figures ranged from about 10 to 15 orders per day at the low end up to a typical 5,000 per day, with a 20,000-per-day peak, at the high end. This is the mid-market band precisely: past what a single spreadsheet operator can hold in their head, short of the volume that justifies an enterprise implementation.

Seasonality shows up as a quantified, recurring stressor. One merchant does roughly 90% of a quarter-million annual orders in a single quarter. Another goes from about 800 orders a month to 5,000 in November and December. A third described volume "tripling or quadrupling during holiday peak." Three merchants stated a growth plan in the same breath as their current number, for example "100 to 200 orders per day now, scaling to 1,000 to 2,000 in six months." The volume that matters to this buyer is often not today's, but December's.

Finding 5: The pain stack, ranked

Across the 75 of 76 conversations with at least one extracted pain point, the themes rank as follows. Extraction figures reflect the prospect's stated pain; transcript figures reflect how often the topic surfaced in the room at all.

| Pain theme | How measured | Conversations |

|---|---|---|

| Spreadsheets / manual process | extraction | 47 of 76 (62%) |

| Barcode / scanning discussed | transcript | 61 of 76 (80%) |

| Multi-warehouse topic raised | transcript | 55 of 76 (72%) |

| Cycle counts / physical inventory discussed | transcript | 39 of 76 (51%) |

| Integration / sync problems | extraction | 27 of 76 (36%) |

| Overselling / stockouts topic raised | transcript | 22 of 76 (29%) |

| Vendor neglect / poor support | extraction | 17 of 76 (22%) |

| Implementation time raised as a fear | extraction | 13 of 76 (17%) |

| Overselling / stockouts as an active pain | extraction (pain) | 12 of 76 (16%) |

| Outgrown / too rigid / can't customize | extraction | 12 of 76 (16%) |

| Multi-warehouse as an active pain | extraction | 11 of 76 (14%) |

| Wrong-item / mis-pick errors discussed | transcript | 9 of 76 (12%) |

Two rows deserve a note. Multi-warehouse is discussed in nearly three-quarters of conversations (72%) but named as an active pain in only 14%, which suggests it is more often a near-future requirement than a present fire. Overselling shows the same shape from the other direction: raised in 29% of rooms, but felt as a top pain in 16%. When it is a pain, it is visceral.

"Main challenges are overselling... We think that we have three items of a specific SKU... when we actually go to that unit to pick up the stock... we find only two, we find only one."

- furniture retailer

"While I'm dealing with... the order of the five extinguishers, someone else is dealing with one too, and we both want to take the five in stock... And when it comes to packing, the guy stares at us and says, well, there's only five."

- fire-and-safety equipment retailer

The vendor-neglect theme is worth isolating because it is a churn signal, not just a pain. When an incumbent stops maintaining an integration, the buyer starts shopping.

"We just don't really feel like they're very interested in updating any software as it relates to Shopify... Their integration exists, but when things break, they break hard."

- hardware and building-products merchant

What buyers run today

Counting the prospect's own stated stack (not tools the vendor raised), the platform landscape is Shopify-led and multichannel:

| Platform | Conversations (prospect-stated stack) | Named anywhere in conversation |

|---|---|---|

| Shopify | 39 (51%) | 59 |

| Amazon | 24 (32%) | 37 |

| eBay | 17 (22%) | 19 |

| QuickBooks | 17 (22%) | 26 |

| ShipStation | 14 (18%) | 15 |

| Excel / Google Sheets as system of record | 14 (18%) | 26 |

| Walmart | 8 (11%) | 9 |

| Magento / Adobe Commerce | 7 (9%) | 28 |

| BigCommerce | 6 (8%) | 12 |

| NetSuite | 3 (4%) | 8 |

QuickBooks deserves its own line. It appears in 26 of 76 conversations (34%), almost always as the accounting system of record that any new platform has to integrate with, and in several cases as the only inventory tool the business currently has. As one merchant put it about QuickBooks for inventory: "it's not very good."

The enterprise names, SAP (8 conversations), NetSuite (8), Oracle (8 by extraction), and Manhattan (7 by extraction), appear frequently, but usually as the rejected pole of the decision: the "too expensive, too legacy" option the buyer is defining themselves against rather than seriously considering. That framing matters more than the raw counts.

What buyers actually pay, and expect to pay

The verbatim budget anchors are the most citable part of this dataset, because they are real numbers attached to real businesses. Every figure below was stated by a prospect in conversation.

- A used-auto-parts reseller expected "$500 to maybe $1,000 a month" and called a $2,500/month flat license "out of my realm in terms of that cost."

- An eCommerce retailer put total current software spend "right between six and 650 a month" across all packages.

- A vending and food-and-beverage distributor benchmarked against Zoho at "a few hundred dollars a month" and declined a $5,000/month quote.

- An online grocery merchant pays for Shopify apps "in the ~$99/month range," called a $2,000/month entry price "way, way above my budget," and proposed roughly $100 per location instead.

- An industrial-equipment manufacturer had "$40,000 allocated" to cover both license and implementation, against an enterprise license starting at $72,000/year.

- Another industrial manufacturer anchored on "$5,000 to $15,000" for off-the-shelf licensing before being walked up to a six-figure first-year total.

- An eCommerce retailer replacing Brightpearl estimated current spend at "$20,000 to $25,000 per year" including connectors, and read a $60,000/year quote as roughly 2.5 to 3 times current spend.

- One merchant reported a ShipHero quote of "$15,000 for a yearly plan, up to 55,000 orders," which they computed as about 60 cents per order and called expensive.

- A field-service company pays "over ten grand" for its incumbent inventory system, which the owner openly questions as "worth the money."

- A multi-store bike retailer pays about $3,400/month for ChannelAdvisor as its product-data hub.

- A fastener distributor cited NetSuite at "$3,500 per additional license" as the reason it was moving toward unlimited-user pricing.

Read together, these anchors define the mid-market's price psychology. The comfortable zone is a few hundred to about $1,500 per month. The line where sticker shock begins is around $2,000 per month, and it gets sharper toward $5,000. Per-license and per-order pricing is read as a penalty for growth, which is exactly the growth these merchants are planning for. Flat-rate pricing that does not punish a good December is the structure they respond to.

Takeaways

If you are a merchant evaluating software

Your situation is more common than the sales process makes it feel. If you are running on spreadsheets, you are in the majority (62%). If you are anchored on a few hundred to about a thousand dollars a month, so is most of the mid-market. Three things separate the buyers in this dataset who chose well:

- Price the December problem, not the March problem. Seasonality was a recurring, quantified stressor in these conversations, and several merchants stated a growth plan in the same breath as their current volume. A tool that fits today's order count and breaks or re-prices at peak is not a fit. Ask how pricing behaves at 3 to 4 times your current volume before you sign.

- Weigh the integration you actually depend on. Vendor neglect of a critical integration (22% of conversations) is one of the loudest reasons merchants leave. When you evaluate a platform, evaluate how it treats the connector you cannot live without, usually your storefront or your accounting system.

- Name your real requirements, including the ones you do not feel yet. Multi-warehouse came up in 72% of conversations but was an active pain in only 14%. The buyers who avoided a second migration were the ones who specified for the warehouse they would open next year, not just the one they run now.

If you are a vendor or an analyst

- The buyer's baseline competitor is a spreadsheet, not another platform. In most conversations the incumbent is manual process, not a rival product. Positioning against named competitors misreads the field; the real switching cost is behavioral.

- There is a hard pricing threshold around $2,000 per month for this segment. Above it, expect an explicit objection more often than not (64% of conversations carried a price objection). Volume-independent pricing consistently reduces that friction.

- Speech-to-text undercounts your competitive mentions. If you are mining sales calls for competitive intelligence, normalize garbled brand names before you trust the counts. In this corpus, raw text missed Cin7 and Linnworks references that structured extraction recovered.

A note on method and motive

SkuNexus recorded these conversations in the ordinary course of its own sales process, which is both the reason this dataset exists and its clearest limitation: every conversation was with one vendor, and every prospect had already decided to shop. We have tried to counter that bias by counting rather than cherry-picking, by reporting the conservative number alongside the generous one, and by keeping the product almost entirely out of the findings. The point of publishing it is not to sell. It is that this is the most detailed public picture we know of what mid-market eCommerce merchants actually say when they sit down to replace the software running their warehouse. If it helps a buyer ask a sharper question, or an analyst check a lazy assumption, it has done its job.

Yitz Lieblich is the Founder and CEO of SkuNexus. He has worked in eCommerce since 2007, founded Web Solutions NYC in 2007, and founded SkuNexus in 2018.

Ready to Transform Your Operations?

See how SkuNexus gives you full control over inventory, orders, warehouse, and shipping.

Schedule a Free Demo →

Yitz Lieblich

CEO & Founder, SkuNexus

Yitz Lieblich is the Founder and CEO of SkuNexus. He has spent 19 years in eCommerce, starting in 2007 when he founded Web Solutions NYC, an eCommerce agency he still leads today. His approach to inventory, order, and warehouse management did not come from a whiteboard. It came from the floor. Across nearly two decades, Yitz has worked with merchants of every size, from mom-and-pop startups to Fortune 100 enterprises, across auto parts, food and beverage, apparel, B2B wholesale, and retail/D2C. He has walked through hundreds of warehouses, watching where operations lose time, money, and orders, with one goal: optimize the operation and make it easier for the merchant. That hands-on pattern is what led him to build SkuNexus in 2018 as a full operational platform. The idea was simple. Configurable infrastructure that bends to each merchant workflow, supporting businesses that ship anywhere from 50 to 20,000 orders a day. A custom development background runs through everything he builds. When SkuNexus writes about fulfillment, WMS, or multi-channel inventory, it comes from operations Yitz has seen and solved firsthand. First as an agency partner since 2007, and now as the architect of the platform.